Wildfire Mitigation & The 2026 Insurance Market: Turning Safety into Savings

In Southern Oregon, "Wildfire Season" is a reality we live with. But for the first time, your efforts to protect your home can directly lower your monthly mortgage payment.

The Legislative Breakthrough: SB 1540

For years, homeowners in the Rogue Valley felt penalized by rising insurance premiums regardless of how much "defensible space" they created. In 2026, the tide has turned. New state mandates (building on the momentum of SB 1540) now require insurance companies to factor property-specific mitigation into their risk models.

This is a game-changer for Southern Oregon real estate. It means that the money you spend on "Hardening your Home" now has a measurable Return on Investment (ROI).

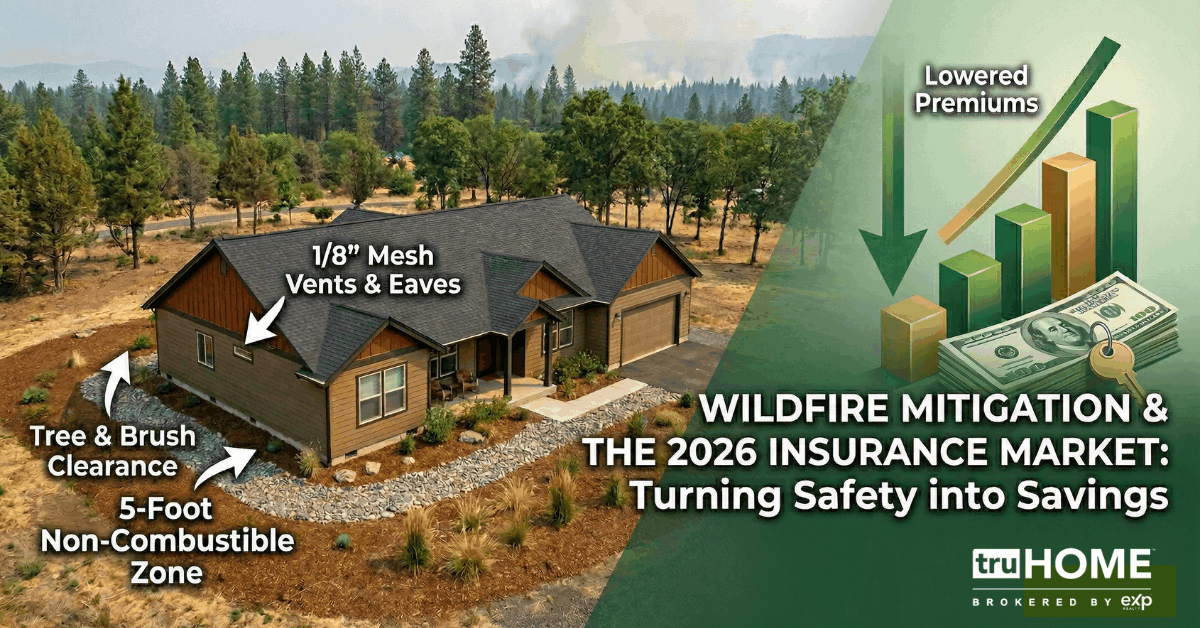

Three Steps to Lowering Your 2026 Premiums

- The 5-Foot Non-Combustible Zone: Replacing wood mulch with river rock and removing flammable shrubs (like juniper) within five feet of your foundation is the highest-weighted factor for many insurers.

- Vents and Eaves: Embers, not walls of flame, destroy most homes. Upgrading to 1/8" mesh non-combustible vents is a low-cost upgrade with high-value insurance credits.

- Community-Level Action: Are you in a "Firewise" community? In 2026, being part of an organized mitigation neighborhood can trigger "Community-Level" discounts that individual homes can't get on their own.

Expert Tip for Sellers: Make a "Fire Resilience Portfolio." Include your receipts for tree thinning, roof cleaning, and vent upgrades. Giving this to a buyer’s insurance agent can be the "deal-maker" that keeps their monthly payment within their budget.

For more valuable tips, please visit: https://truHOME.net

Categories

Recent Posts